SWTCH by Pigment

Three days of predictions, insights, and advice from leaders in finance, sales, HR, supply chain and more

Register now here

SWTCH by Pigment

Three days of predictions, insights, and advice from leaders in finance, sales, HR, supply chain and more

Register now here

A ‘financial’ strategist is a strategist first and a financial second. For decades financials have been applying solutions to become a strategic business partner for the C-suite, from financial engineering and tax planning to centralising (global) operations and deep analytics today. To avoid drilling deeper and still finding nothing, reverse engineering the strategic role of the financial will show another route to be of value and increase the yield on IRR or profits with double digits…

If CFOs and FDs aim to improve the decision-making process by the C-suite, meaning add value to the business, accounting and compliance aren't helping this quest. In fact, if you read the report by the American Institute of CPAs (AICPA) and the Chartered Institute of Management Accountants (CIMA), Joining the Dots: Decision Making for a New Era, you’ll be in shock:

It is all about information, yet more details or more of the same data will give you the same answers, only in more detail or at a higher spend (CapEx). The trick is to reverse the direction the financial is looking: from ‘stargazing into a black hole’ to ‘storytelling based on facts’. For this to happen, the business's strategy needs to be placed into the ‘accounting’ systems.

A simplified example will show how this ‘street smart’ solution was encountered (step 1) and how it is set up (step 2).

A strategy is often a group of plans where the numbers disappear in PowerPoint presentations, Excel sheets or BI software. Many financials are hooked by their screens, yet the story in the plans is ‘lost in translation’.

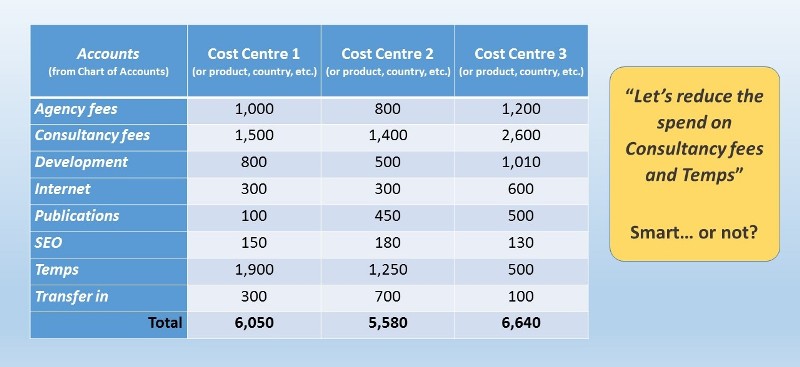

For example, what does the following overview tell you?

Figure 1

Not much; it just shows you the composition of spending, not the strategic intent. As a board member, you might even be tempted to reduce Consultancy fees and Temps as part of a company-wide ‘savings initiative’ in response to market pressures.

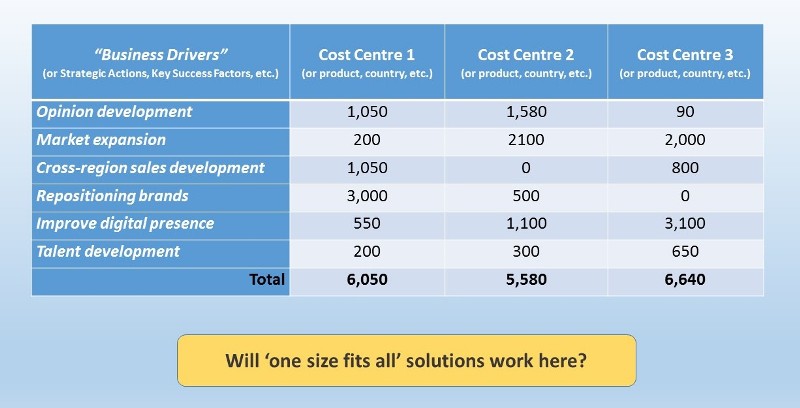

The first step to increasing your understanding is to talk to Sales & Operations and ask what drives and blocks their business. For the same example, the “Accounts” have been decomposed and reshuffled into the “Business Drivers”, showing how each business plan is to be developed.

When the result is lagging, which question will you ask now?

Figure 2

Of course, as a board member, you will ask where and why performance is lagging. This is how the decision quality is increased, avoiding ‘one size fits all’ solutions. And normally, it’s the financials that should have provided the CEO, CFO or GM with the right answer.

As a financial, you have talked to Sales & Operation (managers, directors, and global VPs), who have given you a jointly agreed list of key “business drivers” for each market. This list should match their business plans or strategy. One problem, there are no such descriptions in the Chart of Accounts or as Cost Centres. Here enters project accounting.

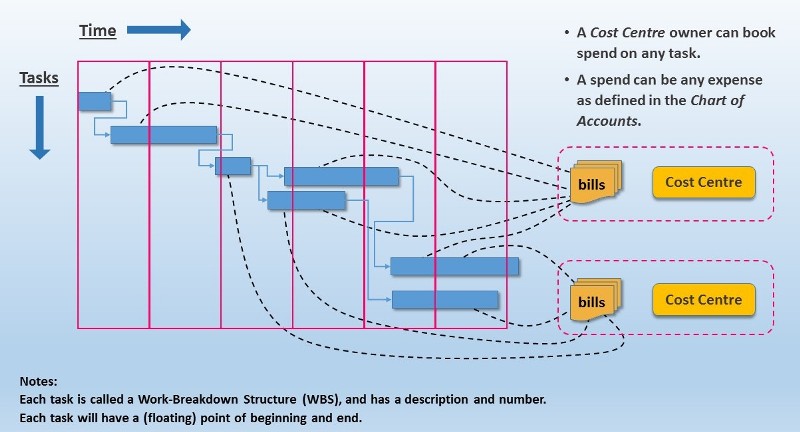

What is a project? Basically, it is a sequential flow of various tasks. Each project task can contain any kind of spending, following the Chart of Accounts, and different ‘Cost Centres’ can book a project activity when working (or purchasing) together.

Standard project:

Figure 3

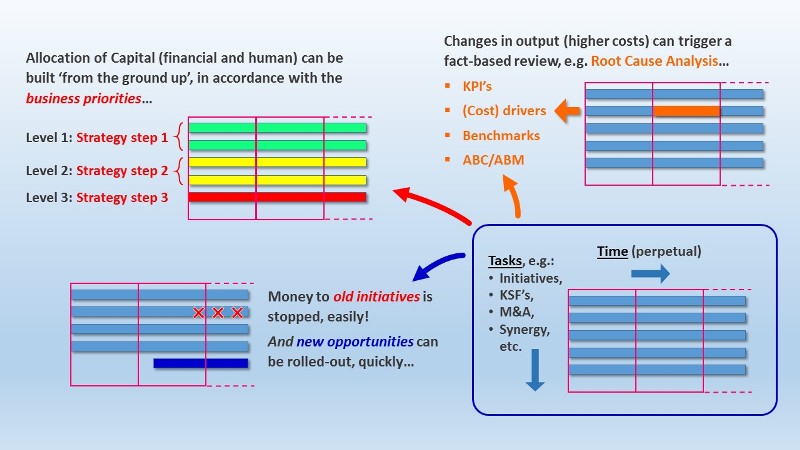

Within project management, each project task or activity is called a Work-Breakdown-Structure (WBS), with a WBS description and WBS number. To transform project accounting into a strategy storyboard, you give each project task a WBS description of a “business driver” and have a term which lasts, e.g. 20 years or more. Now the strategy is in the accounting system!

Strategy storyboard:

Figure 4

The only instruction you have to give the budget owners is that their assistant books each transaction and allocation with one additional code: the WBS number, which is given by the budget owner and related to one of the business drivers.

Now that you have the strategy translated into a storyboard in your accounting system and the amount is being booked, this is what you get:

Project accounting has more reporting advantages, e.g. it ‘overwrites’ / no cross-border limits, bookings can be split between different WBS numbers, and various consolidation hierarchies are possible.

A company using a traditional business planning method will learn quickly. After management sees where the money really went and notices they spent less time understanding the numbers, they will permanently reduce spending on non-value-added activities and fund only the best new opportunities.

Those companies familiar with Beyond Budgeting, Driver-Based Planning, or (strategic) Zero-Based Budgeting will immediately see the real advantages:

The increase in returns comes from the effective execution of the strategy and adapting it in accordance with the business environment. By linking the strategy with accounting, and not the other way around (!), project accounting is writing the real success story every month!

Independent of the accounting, ERP or BI system installed, using project accounting can turbocharge any financial into a strategic business partner without the need for any significant investment. The link to strategic planning becomes evident when FP&A is placed within this bigger picture. By translating the strategic intent of the company into business drivers made visible through the ‘use-of-funds’, the execution of the strategy becomes fact-based, transparent and verifiable: ‘talks & figures’. Just think about it, and add value to your role and company.

It is very important to have well-established mechanisms for planning and budget control. So, managers can...

Best practices from mature technology businesses have stable recurring Rolling Forecasts based on momentum, executive buy-in...

Strategy execution means core competencies support a realistic strategy and that the plan can be achieved...

Does your organization’s strategy seem like a mystery or carefully guarded secret? Can it feel as...

We will regularly update you on the latest trends and developments in FP&A. Take the opportunity to have articles written by finance thought leaders delivered directly to your inbox; watch compelling webinars; connect with like-minded professionals; and become a part of our global community.